UK mortgage rates October 2025: Just when homeowners were starting to breathe easier, mortgage rates have crept back up. For the first time since February, the average UK mortgage rate has risen slightly, reminding borrowers that the calm in the housing market might not last forever.

According to new data from Moneyfacts, both two-year and five-year fixed-rate mortgages have nudged higher this month. It’s not a dramatic jump — just 0.02 percentage points — but after months of steady declines, this tiny uptick is enough to make borrowers pause and lenders cautious.

So, what’s really going on here? Let’s break it down.

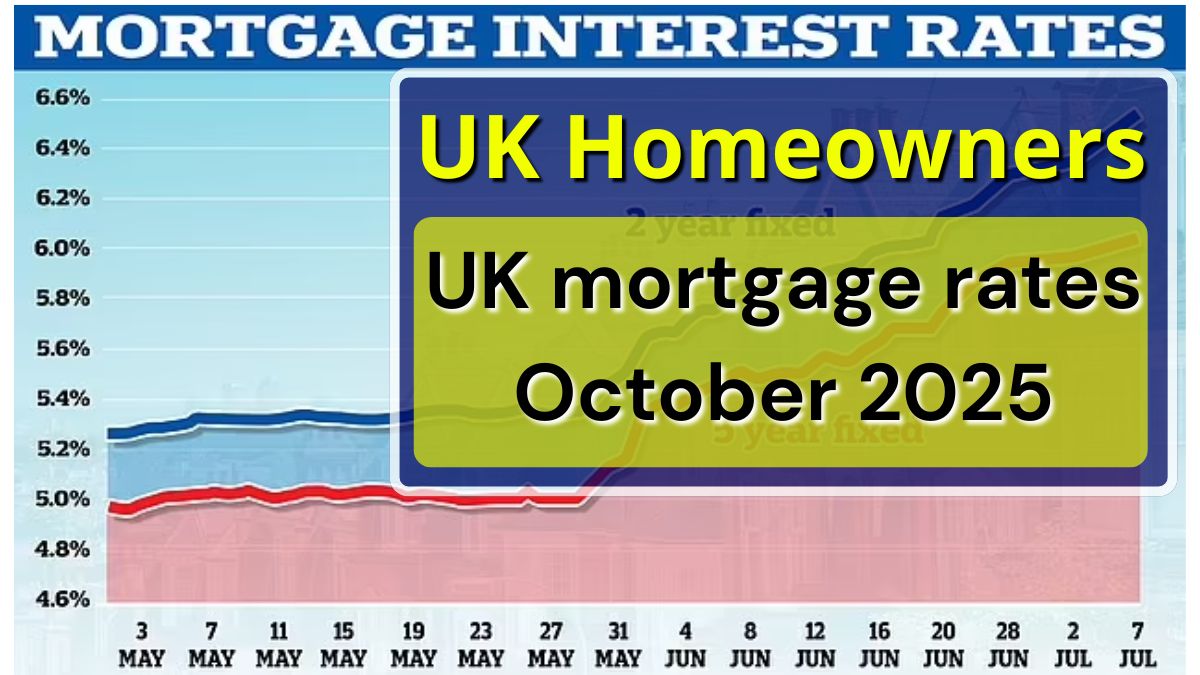

Average Mortgage Rates: Small Change, Big Meaning

The average two-year fixed mortgage now sits at 4.98%, while the average five-year fixed deal is around 5.02%.

On paper, those numbers are much better than the painful highs of 2023, when some borrowers were staring down rates of 6.67% or more. But for many homeowners and first-time buyers, these levels are still tough — especially after years of ultra-low rates in the 2010s.

Think about it: someone who once paid 2% interest on a £200,000 mortgage would now be paying hundreds of pounds more each month. Combine that with higher grocery and energy bills, and you can see why households are feeling the squeeze.

Why the Sudden Change?

Experts say the rise isn’t about panic — it’s about caution.

Rachel Springall from Moneyfacts explains that “volatile swap rates and a cautious approach among lenders have led to an abrupt halt in consecutive rate drops.”

Here’s what that means in plain English: lenders set their mortgage rates based on swap rates, which reflect where the market thinks the Bank of England’s base rate is headed. If there’s uncertainty about future cuts or the upcoming Budget, lenders tend to play it safe — adjusting rates slightly higher to protect themselves.

And that’s exactly what’s happening now.

Are Base Rate Cuts Still Coming?

Some analysts had expected the Bank of England to start trimming rates before the end of the year. But those hopes are fading.

“Further base rate cuts appear unlikely in the immediate future,” Moneyfacts noted. And since uncertainty often builds before a national Budget, it’s natural for lenders to hit pause.

Simon Gammon, managing partner at Knight Frank Finance, says this doesn’t mean we’re heading back to sky-high borrowing costs:

“This is unlikely to mark the start of a sustained rise in borrowing costs, but rather a prolonged plateau while the outlook becomes clearer.”

In short, the market isn’t crashing — it’s holding its breath.

What This Means for You

If you already have a fixed-rate mortgage, you’re safe for now. More than 80% of UK homeowners are on fixed deals, which means their monthly payments won’t change until their term ends.

But if your deal is due to expire soon — or you’re a first-time buyer — this slight increase could mean paying a little more than expected.

Here’s the smart move: don’t rush into locking in a new rate just because of rumours about the Budget or future rate changes. As Springall advises, “Borrowers should consider their own circumstances and seek independent advice to navigate the mortgage maze.”

That’s good advice — especially since lenders might adjust deals again once the Budget’s direction becomes clearer in November, when Chancellor Rachel Reeves is expected to announce new measures.

The Bigger Picture

Even with this small increase, today’s mortgage rates are still much lower than they were two years ago. For many, that’s a silver lining.

But it’s also a reminder that the era of ultra-cheap borrowing is over — at least for now. As the Institute for Fiscal Studies (IFS) warned this week, the government should avoid “half-baked fixes” in its Budget and instead focus on sustainable, long-term solutions that keep housing affordable.

Until then, both homeowners and would-be buyers should stay informed, plan ahead, and avoid panic moves. Sometimes, patience pays more than prediction.

Frequently Asked Questions

1. What are the current average UK mortgage rates?

As of October 2025, the average two-year fixed mortgage rate is 4.98%, and the five-year average is around 5.02%, according to Moneyfacts.

2. Will the Bank of England cut interest rates soon?

Analysts suggest that further rate cuts are unlikely before the November Budget, as uncertainty keeps lenders cautious.

3. Should I fix my mortgage now or wait?

If your mortgage deal is ending soon, compare rates and seek independent advice. Don’t rush based on Budget rumours — lenders often adjust offers afterward.

Join WhatsApp

Join WhatsApp